Here’s a reader question that captures the way a lot of people think about real estate as an investment, especially in big cities. “My husband and I have a block of cash ($200,000) – not enough to buy real estate here in Toronto where we live. How else can we invest with similar returns?”

Good news – getting similar returns to real estate is easy right now. Toronto home prices gained 1.6 per cent on average in February compared with the same month last year. A high-interest savings accounts could have made you 2.3 per cent over the past 12 months, with zero risk. In Vancouver, prices fell nearly 10 per cent in February. Across the country last month, average prices fell 5.2 per cent on a year-over-year basis.

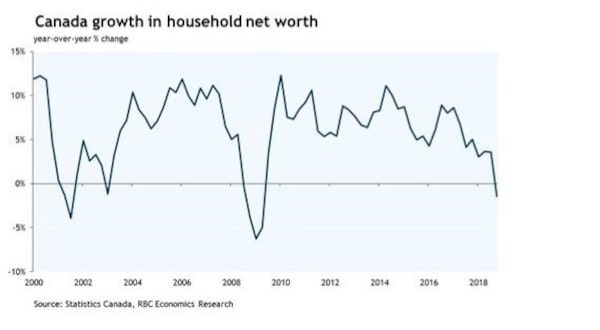

Real estate has without question been a good long-term holding. The average house price in Canada has gone up about 5.4 per cent annually on average since 1990, figures from the Canadian Real Estate Association show. The past several decades have been a time of steadily falling interest rates – that’s a huge support to house prices. But with rates close to the bottom now, future prospects for house prices have to be tempered. In a recent report, RBC Economics looked at slowing housing markets and said “a golden decade for household wealth creation is coming to an end.” Check out this chart on growth in net worth, which was boosted in previous years by house price gains:

Now, let’s say that past 5.5-per-cent return from housing annually is still feasible. Can you match it with conventional investments? The answer is very likely yes, if you build a diversified portfolio of mainly stocks but also bonds.

One final note: Houses have a tax advantage over conventional investments made outside registered accounts such as RRSPs and TFSAs in that you can sell a principal residence tax-free. Here’s a guide on how real estate is taxed in other circumstances.

Subscribe to Carrick on Money

Are you reading this newsletter on the web, or did someone forward the e-mail version to you? If so, you can sign up for Carrick on Money here.

Rob’s personal finance reading list …

The bucket list travel guide to using credit card reward points

Five great vacation spots and how to get there as cheaply as possible using points from various credit card travel reward programs.

Happiness and Money, Part One

A Harvard Business School professor argues you can make yourself happier by spending money to eliminate your most stressful tasks in life. The problem: People feel guilty about spending money to have their laundry washed and folded, or their meals delivered.

Happiness and Money, Part 2

A Q&A with Melissa Leong, money expert on The Social (CTV) and author of the book Happy Go Money. This strikes me as a good idea: “I give myself a spending account that gives me the freedom to buy things that make me happy.”

Nextovers, not leftovers

The nextover is a breakthrough in frugal cooking. When preparing a meal, make extra of one key component – veggies, grains such as rice – and then use it as the base for your next meal.

Today’s financial tool

Find out how much bigger your returns could be if you lowered the investment fees you pay.

What I’ve been writing about

- Four reasons why you might not get the great mortgage rate you saw online

- It’s time to stop pretending RRSPs are a universal retirement-savings vehicle

- Rob Carrick’s 2019 ETF Buyer’s Guide: Best global equity funds (for Globe Unlimited subscribers)

More Carrick and money coverage For more money stories, follow me on Instagram and Twitter, and join the discussion on my Facebook page. Millennial readers, join our Gen Y Money Facebook group. Send us an e-mail to let us know what you think of my newsletter. Want to subscribe? Click here to sign up.

Rob Carrick

Rob Carrick