'Payback'

Several of Canada’s housing markets lost some steam in January, hot on the heels of a new report that warns of a cooling-off period.

Or, as Toronto-Dominion Bank put it in a fresh forecast, some “payback” after the exceptional boom years.

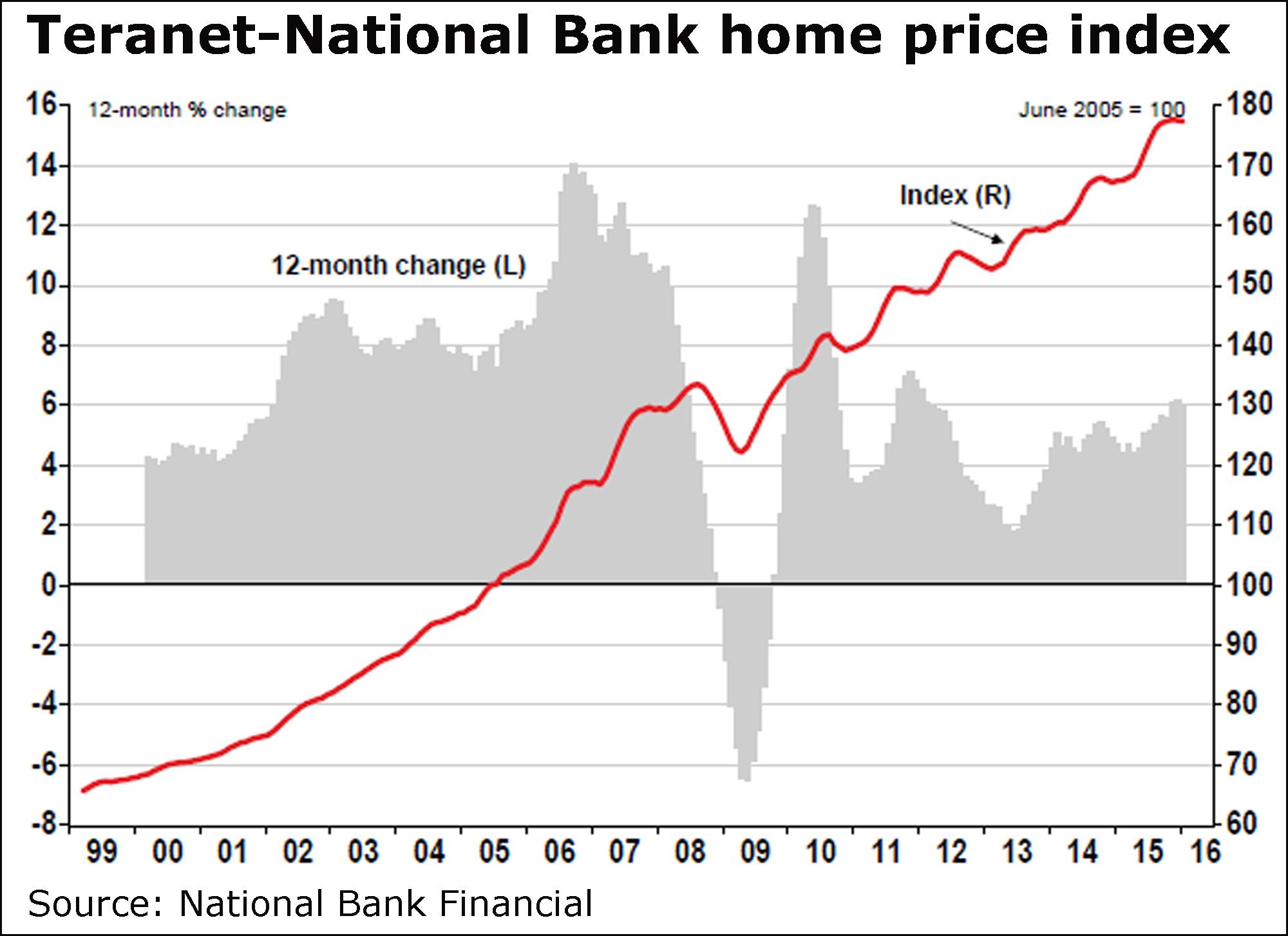

According to the Teranet-National Bank home price index released today, values across the country dipped 0.1 per cent in January from December, marking the second decline in a row.

On a year-over-year basis, they were still up 5.9 per cent, which the group called a “quite respectable gain,” albeit the slowest in three months.

Prices slipped from December to January in Montreal, the Ottawa region, Calgary, Edmonton, Quebec City, Toronto and Halifax.

“The report confirms that housing markets in oil-dependent regions are reacting to the economic downturn resulting from the collapse of oil prices,” said National Bank senior economist Marc Pinsonneault, citing the four-month string of losses in Calgary.

Take note that the monthly decline in Toronto was the first in almost a year.

But other markets are still going strong, including Vancouver, Victoria and Winnipeg.

Several cities chalked up some big annual gains, specifically Vancouver, at 12.5 per cent, Hamilton at 10.3 per cent, Toronto at 8.6 per cent, and Victoria at 8.5 per cent.

Those happen to be the cities that TD warned about in its new forecast this week.

Just to be clear, TD economist Diana Petramala isn’t calling for a meltdown, but rather lower gains this year and marginal declines in 2017.

Some mortgage rates are on the rise, which could continue, coupled with the federal government’s new mortgage insurance rules, she noted.

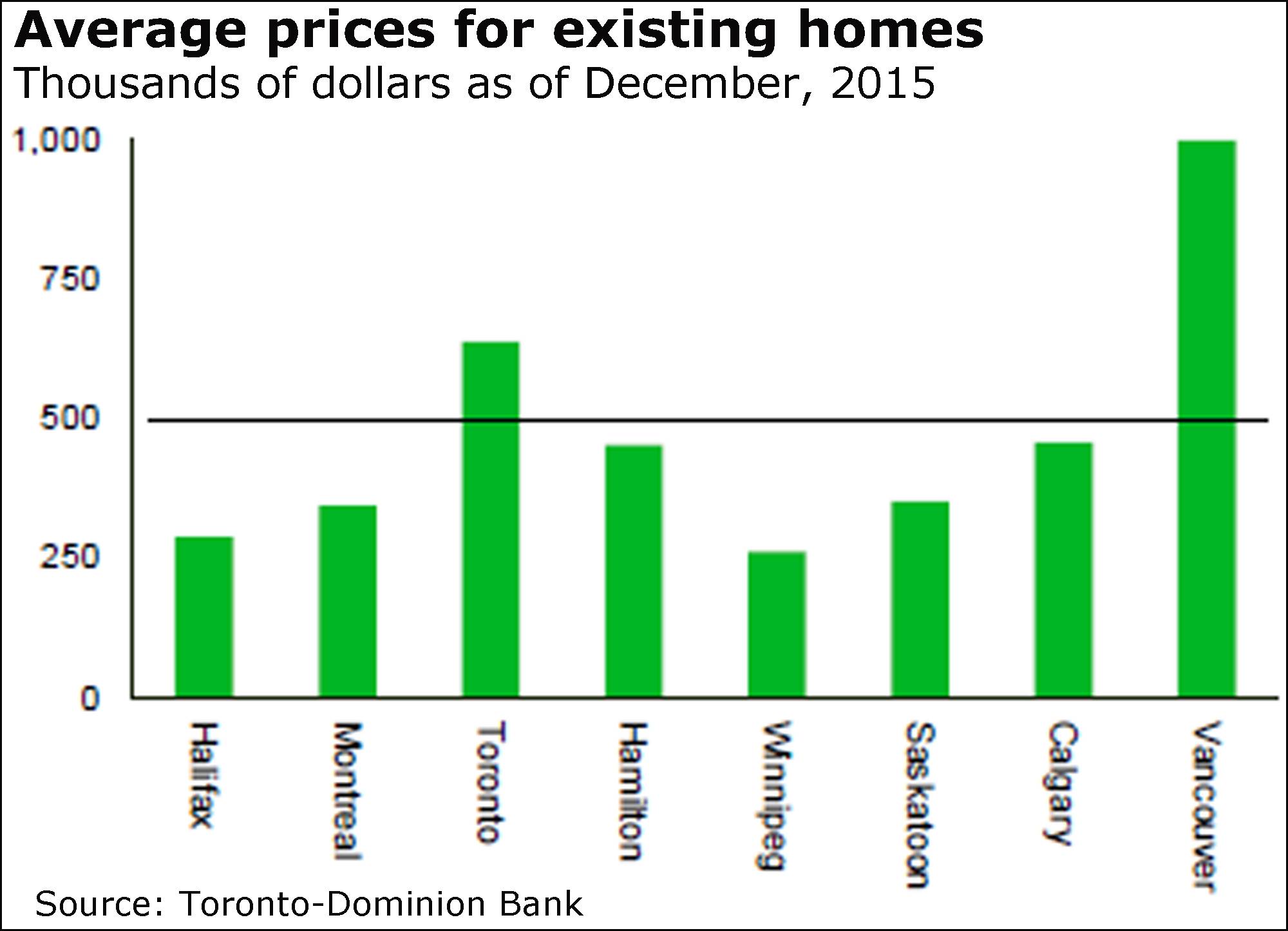

The focus in Canada has been on Vancouver and Toronto, which have racked up gains, stretching affordability and sparking controversy.

“The lofty activity last year has likely left these two markets more vulnerable to even a gradual increase in interest rates and regulatory rule changes,” Ms. Petramala said.

“Average existing home sales and new home construction may ease off record levels through 2016 and 2017, but still remain above their long-run average,” she added.

“The Vancouver housing market, in particular, is the most volatile of the 13 markets, with some payback following banner years quite common.”

Ms. Petramala projected slower average price gains of about 4 per cent in Toronto this year, followed by a modest drop in 2017.

She also forecast 2016 gains of 7 per cent, followed by a 2-per-cent decline next year.

But it’s not just Toronto and Vancouver.

Certain nearby centres have also been “sizzling,” Ms. Petramala noted, and price increases will be moderate this year and next.

“In particular, Victoria and Hamilton enjoyed equally sized gains in housing demand last year as Toronto and Vancouver,” she said.

“As such, these markets may see some payback in 2016 and 2017 as market activity overall eases off elevated levels,” she added.

“However, they will continue to remain affordable when compared to their bigger city counterparts, which will make them more attractive to first-time homebuyers.”

National Bank’s Mr. Pinsonneault noted that Toronto, Hamilton, Vancouver and Victoria were the sole drivers of the overall annual increase.

“With population and job growth in these markets continuing to exceed the national average for the foreseeable future, a major price correction is unlikely in these markets,” he added.

Quote of the day

“Gold bugs might well have been pinching themselves yesterday to ensure it wasn’t all a dream.”

Alastair McCaig, IG

Some European nations stagnate

Europe’s markets may be rallying today, but some of its economies are something else entirely.

The economies of the euro zone and the broader European Union expanded by 0.3 per cent in in the fourth quarter of last year, according to numbers released today by the Eurostat statistics agency.

But you can see the wide differences when you dig deeper.

Among the major euro zone countries, Germany pulled the group ahead with growth in gross domestic product of 0.3 per cent. But France and Italy lagged, at 0.2 per cent and 0.1 per cent, respectively.

Britain, which is not part of the monetary union, came in at 0.5 per cent.

And Greece, ever the basket case, saw its economy shrink by 0.6 per cent.