Briefing highlights

- How bloody could a correction be?

- All eyes on Trump address tonight

- Scotiabank boosts dividend

- BMO posts stronger profit

How bloody?

The chorus of voices warning of a potential stock market pullback is echoing around the world.

Which suggests the next question may well be: How bloody could it get?

It needn’t be too severe, some observers say, but so much remains unknown because Donald Trump has yet to unveil certain details of fiscal policy well beyond what he flagged on Monday, saying he would boost defence spending and cut money for foreign aid, among other things.

Thus, all eyes will be on Mr. Trump later in the day when he addresses a joint session of Congress, providing an opportunity to elaborate on tax, trade and other fiscal issues.

For now, investors are on a sugar high the likes of which have rarely been seen before in a postelection period. Yet an increasing number of analysts are considerably wary of what comes next amid vague and, at times, contradictory signals from Washington.

“Naturally, the dizzying heights for equities are causing some vertigo, with a wide variety of commentators and analysts openly fretting that the market is overbaked,” said Bank of Montreal chief economist Douglas Porter.

“That’s especially the case when there is still so much uncertainty surrounding both the content and the timing of any potential changes in U.S. tax policy and the regulatory environment.”

And, of course, it’s not just the United States. There’s Brexit and the rise of Marine Le Pen in France, just for example.

In the U.S., the last long winning streak for the Dow Jones industrial average came in 1987, noted John Higgins, the chief markets economist at Capital Economics, projecting a “sharp fall” in the U.S. benchmark, though not particularly soon.

For anyone not yet born, that’s when a crash, which started on Black Monday, wiped 36 per cent off the Dow over the course of a couple of months.

“Looking ahead, we think that bond yields will rebound, while equity prices will falter,” Mr. Higgins said in a separate report Monday.

“We think that some of the heat is likely to come out of equities, whose valuations are now looking quite stretched,” he added.

“Even if there is an eventual boost to earnings from lower taxes, we suspect that it will be largely offset by a drag from higher wages and further strength in the dollar.”

Mr. Higgins believes the S&P 500, which closed Monday just shy of 2,370, will “edge down” to 2,300 by the end of the year.

Similarly, Goldman Sachs said in a fresh forecast that it expects the S&P 500 to peak this quarter at 2,400, slipping to 2,300 by year end, though the big U.S. bank didn’t go beyond 2017.

Morgan Stanley, in turn, having studied several measures, says there are signs both bad and good.

“Risk assets and macro metrics give mixed signals about the chance of a large drawdown in the next 12 months, with the average odds close to what’s ‘normal’ (18 per cent),” it said in a study.

“Real yields, oil and equity valuations are flagging a higher risk (30 to 40 per cent) [of a correction], while credit is more sanguine.”

So if it happens, when might that be?

Most bear markets come amid recessions, when corporate earnings slump, said Mr. Higgins. And at this point, Capital Economics doesn’t see a near-term recession in the cards.

“Indeed, we think that the U.S. economy will fare quite well over the next year or two,” he said.

“Further ahead, though, things are likely to get bleaker for equity investors. The fiscal boost to economic growth should have faded by that point and monetary policy is likely to be a lot tighter than it is now. The risk of a recession will therefore be high.”

Like Mr. Higgins, other analysts also cite a solid economy at this point, one inherited by Mr. Trump, and strong signs from the latest earnings.

“However, it is notable that the policy uncertainty is casting much more caution on bonds and the U.S. dollar than it is on stocks,” Mr. Porter said.

“It’s hard to believe that the separation will last much longer, especially as details emerge in coming weeks/months on the U.S. fiscal policy front.”

Noting that U.S. stocks “ain’t dirt cheap,” Canadian Imperial Bank of Commerce chief economist Avery Shenfeld nonetheless cited reasons for a not-too-bad market slump.

“We’re not big believers in the idea that the new administration in Washington will be able to significantly accelerate economic growth,” Mr. Shenfeld said in a recent report.

“But there are reasons why stocks should carry a higher-than-average multiple on one-year-ahead earnings,” he added.

“After all, no Finance 101 prof ever taught you to value a stock based on one year’s earnings. So what counts is not just 2017, but what comes after that. We don’t know the details yet, but odds are that both corporate tax and regulatory compliance costs will be lighter in the U.S. come 2018, savings that should flow through to profits and share values.”

True, the U.S. expansion has been running for some time now, and perhaps a recession is in the offing.

Ah, but, Mr. Shenfeld noted, postwar expansions have ended because of oil shocks or “the late stages” of a cycle of interest rate hikes, rather than length of time.

Another oil shock is unlikely at this point, and U.S. rates are, of course, still low even though they’re rising.

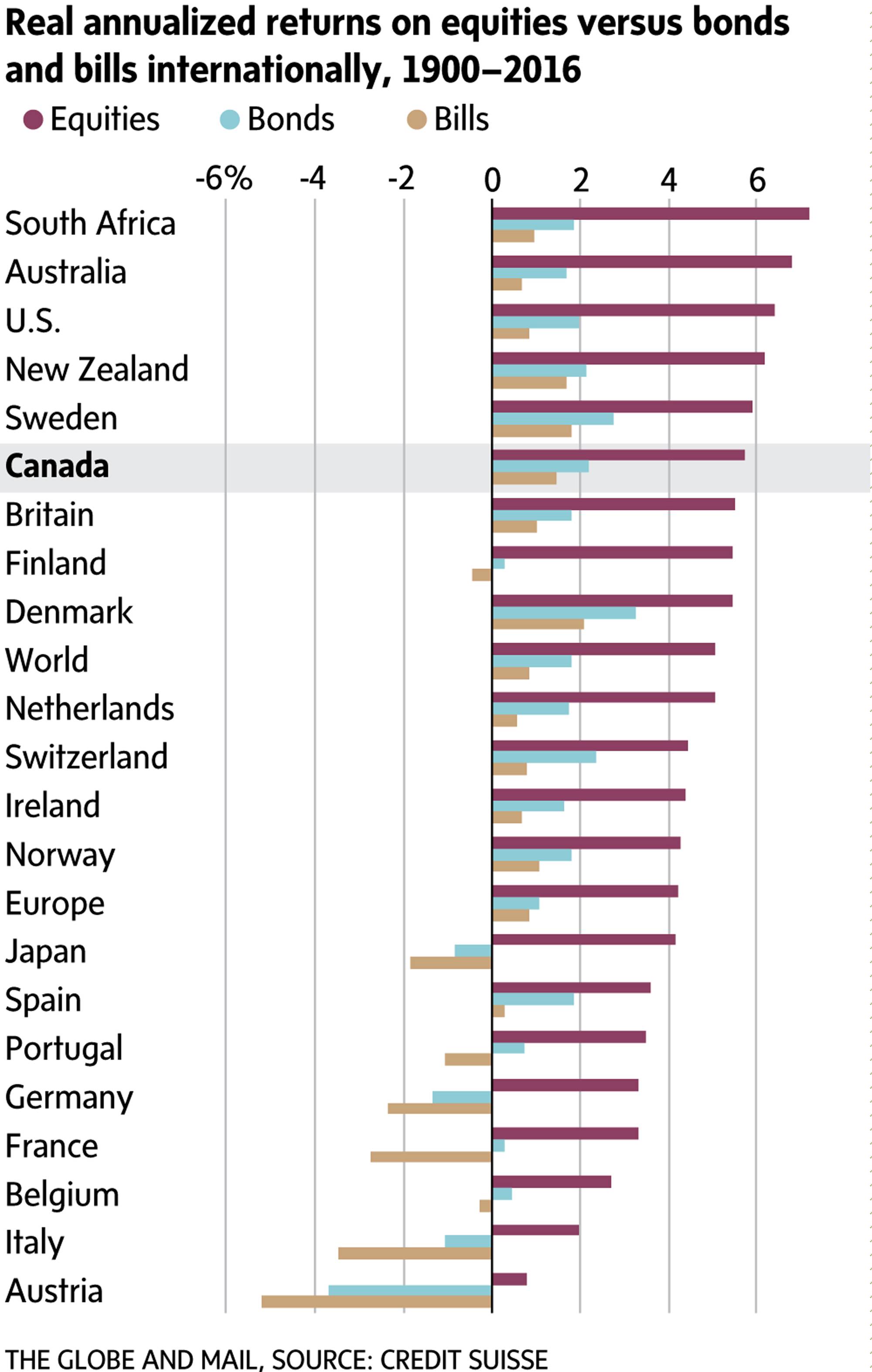

Here, for the record, is a look by Credit Suisse at very long-term stock market performances.

What to watch for today

It’s all about what Mr. Trump signals in his speech, and what particulars investors take away from it, given that, so far, his promises lack details and some signs from the White House have been contradictory.

“USD bulls are hoping for greater specifics on tax reform, infrastructure spending, or at least a sense of what will be prioritized,” said Bipan Rai, CIBC’s executive director of macro strategy, referring to the U.S. dollar by its symbol.

There’s a lot at play but markets will be looking specifically at whether a so-called border adjustment tax, an initiative of congressional Republicans rather than the administration, becomes part of official trade policy, Mr. Rai said.

“Ahead of the speech, the odds don’t look so good as Trump’s own chief economic adviser (Gary Cohn) has indicated that the White House would not support the measure on Friday,” he added.

“Last week’s message from Treasury Secretary [Steven] Mnuchin was also telling. In addition to looking towards 3-per-cent growth in the latter half of 2018, more details on tax reform may not be available until August. Those comments were a serious blow to the USD in the near-term.”

Bank dividends roll in

Bank of Nova Scotia is the latest among Canada’s biggies to boost its dividend amid higher first-quarter results.

The quarterly payout rises 2 cents to 76 cents, following dividend increases last week from Canadian Imperial Bank of Commerce and Royal Bank of Canada.

Scotiabank also posted a profit of $2-billion, or $1.57 a share, up from $1.8-billion or $1.43 a year earlier.

Bank of Montreal, meanwhile, stands alone among the majors so far, with no boost to its dividend but matching the trend for higher profits.

BMO profit rose in the first quarter to $1.49-billion, or $2.22 a share, from $1.07-billion or $1.58 a share earlier.

The bank also announced plans to buy back up to 15 million common shares.

BMO’s provisions for credit losses edged down to $173-million from $183-million.